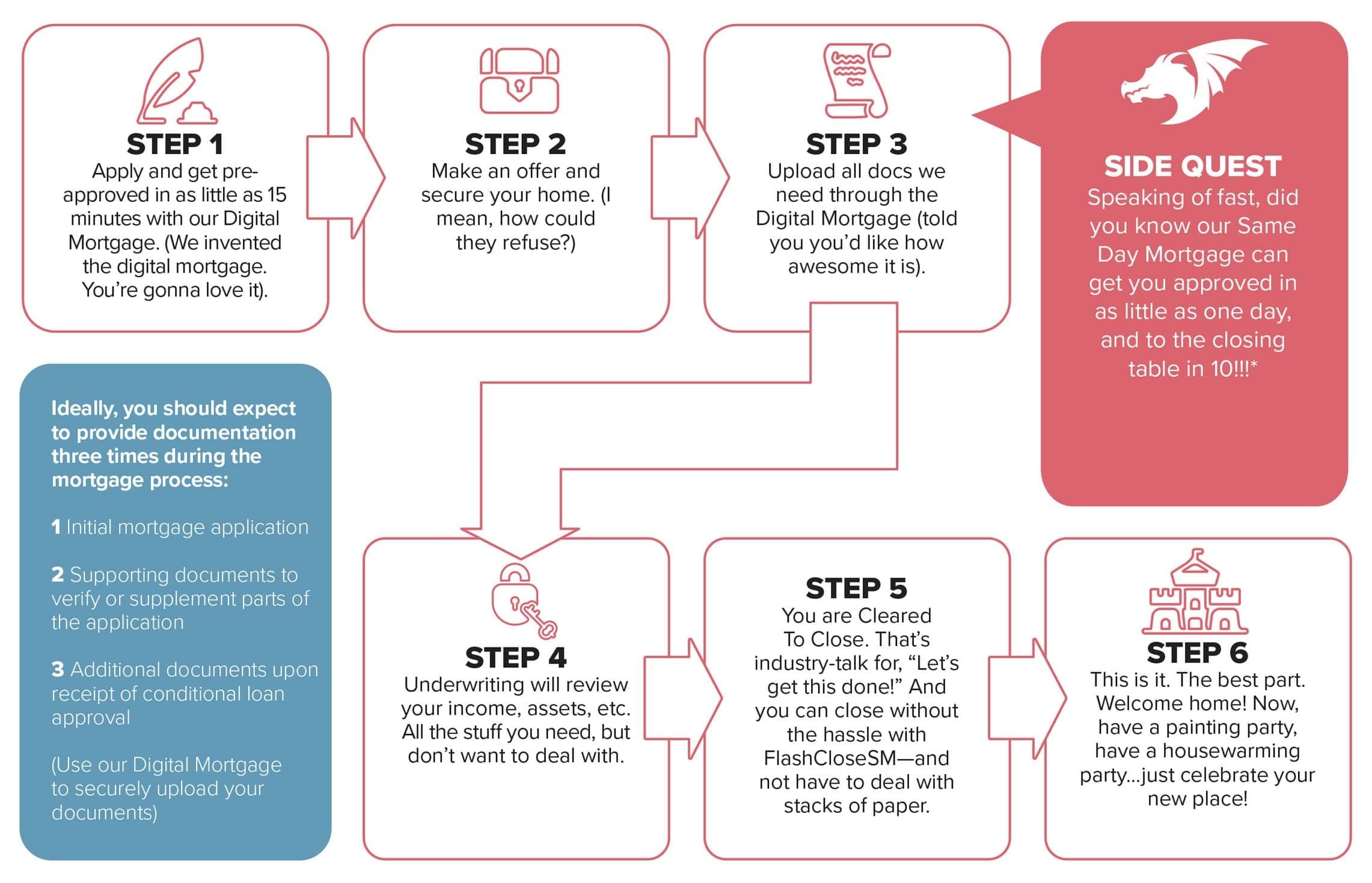

Introduction

The mortgage application process is often seen as complex and intimidating, but it is a crucial step in purchasing a home. Understanding the process can help streamline your journey toward homeownership. With recent changes in lending standards, market conditions, and the digitalization of the mortgage industry, the process may vary slightly depending on where and how you apply. This step-by-step guide will walk you through the typical process and provide insights on recent trends and research.

Step 1: Assess Your Financial Situation

Before you even think about applying for a mortgage, it’s essential to understand your financial health. This includes reviewing your income, debt, savings, credit score, and any other financial obligations.

Key Considerations:

- Credit Score: A good credit score is critical to securing favorable mortgage terms. Most lenders prefer a credit score of at least 620 for conventional loans, but a score of 740+ can help you get the best interest rates.

- Debt-to-Income (DTI) Ratio: Lenders assess your monthly debt obligations in relation to your income. A DTI ratio of 43% or lower is generally considered ideal, but some programs allow for higher ratios.

- Down Payment: The larger your down payment, the better your loan terms might be. Typically, a down payment of at least 20% is recommended, though some programs allow for as little as 3% down.

Step 2: Research Mortgage Types

There are several types of mortgage loans, each with its own set of eligibility requirements, interest rates, and terms. Researching these options will help you determine which one fits your needs best.

Common Mortgage Types:

- Conventional Loans: These are not insured by the government and typically require a higher credit score and down payment.

- FHA Loans: Backed by the Federal Housing Administration, these loans are available to borrowers with lower credit scores and smaller down payments.

- VA Loans: Available to veterans, active-duty military members, and some surviving spouses, VA loans often require no down payment and offer favorable interest rates.

- USDA Loans: For rural and suburban homebuyers, these loans offer no down payment and low interest rates but come with specific eligibility requirements related to income and location.

Step 3: Pre-Approval vs. Pre-Qualification

Before formally applying for a mortgage, you may want to get pre-approved or pre-qualified for a loan.

Pre-Qualification:

- A pre-qualification is a less formal process where the lender estimates how much you could borrow based on a self-reported assessment of your finances.

- It is a good first step to understand what you can afford but carries no weight in the eyes of sellers.

Pre-Approval:

- A pre-approval is a more formal process. It involves the lender reviewing your financial documents (like your credit score, income, and debts) and issuing a letter stating how much they are willing to lend you.

- Having a pre-approval letter can give you a competitive edge when bidding on homes, as it shows sellers you are a serious buyer with the financial backing to make a purchase.

Step 4: Submit the Application

Once you have selected your lender and mortgage type, it’s time to submit a formal application. This will involve providing comprehensive details about your finances, employment, and the property you are purchasing.

Key Documents You’ll Need:

- Proof of income (pay stubs, tax returns, etc.)

- Credit report (provided by the lender)

- Bank statements and asset documentation

- Personal identification (e.g., driver’s license, Social Security number)

- Details about the property (in the case of a specific home purchase)

Step 5: Mortgage Processing and Underwriting

After you submit your application, the mortgage lender will process your documents and begin the underwriting process.

What Happens During Underwriting?

- The underwriter reviews all your submitted documents, verifies their accuracy, and assesses whether you meet the lender’s criteria.

- The underwriter will also evaluate the property you are purchasing through an appraisal to ensure it is worth the loan amount.

- The lender may request additional documentation or clarification during this phase.

Step 6: Mortgage Approval or Denial

Once underwriting is complete, the lender will either approve or deny your application. If approved, the lender will send you a loan commitment letter outlining the terms of your mortgage (loan amount, interest rate, monthly payments, etc.).

What If You’re Denied?

- If you are denied, it is essential to understand the reasons why. Common reasons include a low credit score, high debt-to-income ratio, or insufficient documentation.

- You can often address these issues, whether by improving your credit score, paying down debt, or submitting additional documentation.

Step 7: Closing the Loan

The final step in the mortgage application process is closing. During closing, you will sign the loan documents, and the funds will be disbursed to finalize the purchase of the property.

What Happens at Closing?

- Review of Closing Disclosure: The lender will provide a Closing Disclosure (CD) form, which outlines the final terms of your mortgage, including fees and interest rate.

- Signing Documents: You’ll sign the loan documents, which legally obligate you to repay the mortgage according to the agreed-upon terms.

- Down Payment: You’ll also need to provide the down payment (if applicable) at this stage.

- Receiving the Keys: Once everything is signed and funds are disbursed, you will officially take ownership of the property.

Recent Trends and Research in the Mortgage Industry

1. Digital Mortgage Applications

Recent research indicates a significant shift toward digital mortgage applications. According to the Mortgage Bankers Association (MBA), approximately 70% of borrowers begin the mortgage process online. Many lenders now offer fully digital platforms that allow users to apply for a loan, upload documents, and track the process from start to finish. This trend, accelerated by the COVID-19 pandemic, is expected to continue as lenders invest in user-friendly technology.

2. Increased Focus on Automation and AI

Automation is playing a growing role in underwriting and processing mortgages. Advanced algorithms can quickly evaluate applications and predict loan approval, streamlining the process for both lenders and borrowers. AI is also being used to analyze risk, predict interest rates, and offer personalized loan products.

3. Alternative Credit Scoring Models

While FICO scores remain the industry standard for credit evaluation, there is increasing interest in alternative credit scoring models. Fannie Mae and Freddie Mac have explored incorporating rent and utility payments into credit scoring, allowing more people with thin or no credit files to qualify for mortgages.

4. Growing Popularity of Hybrid Mortgages

Hybrid mortgage products, which combine aspects of both fixed-rate and adjustable-rate mortgages (ARMs), are gaining traction. These loans offer a fixed interest rate for an initial period (e.g., 5, 7, or 10 years), after which the rate adjusts periodically. They are particularly attractive in a rising interest rate environment.

Conclusion

The mortgage application process may seem daunting, but understanding the steps involved and staying informed about the latest trends can make a significant difference. By thoroughly assessing your financial situation, researching mortgage options, and staying organized during the application process, you can increase your chances of securing the right loan for your home purchase.